| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Topic Forums » Economy |

|

| Phred42

|

Mon Dec-15-08 09:59 AM Original message |

| A Second Mortgage Disaster On The Horizon? |

| Printer Friendly | Permalink | | Top |

| bdamomma

|

Mon Dec-15-08 10:00 AM Response to Original message |

| 1. we all better hang on this is going to be a bumpy ride. |

| Printer Friendly | Permalink | | Top |

| kirby

|

Mon Dec-15-08 10:13 AM Response to Original message |

| 2. While everyone likes to blame the poor |

| Printer Friendly | Permalink | | Top |

| CoffeeCat

|

Mon Dec-15-08 10:37 AM Response to Reply #2 |

| 6. I agree with you... |

| Printer Friendly | Permalink | | Top |

| Blue Meany

|

Mon Dec-15-08 01:02 PM Response to Reply #6 |

| 9. My experience is similar... |

| Printer Friendly | Permalink | | Top |

| Trajan

|

Mon Dec-15-08 10:17 AM Response to Original message |

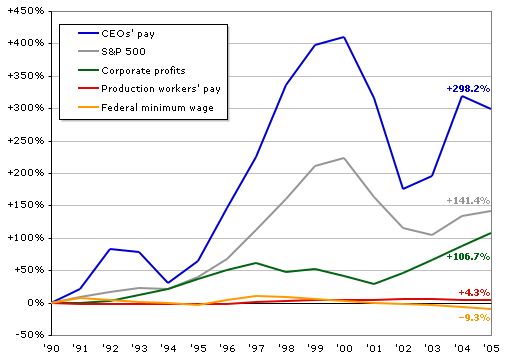

| 3. It is an income issue as well as a loan issue .... |

| Printer Friendly | Permalink | | Top |

| Phred42

|

Mon Dec-15-08 10:37 AM Response to Reply #3 |

| 5. Correct - here's a graph that shows it |

| Printer Friendly | Permalink | | Top |

| kirby

|

Mon Dec-15-08 11:05 AM Response to Reply #5 |

| 7. Looking at your graph? |

| Printer Friendly | Permalink | | Top |

| Phred42

|

Mon Dec-15-08 01:20 PM Response to Reply #7 |

| 10. This one isn't mine. |

| Printer Friendly | Permalink | | Top |

| girl gone mad

|

Sat Dec-20-08 08:54 PM Response to Reply #7 |

| 15. People bought because prices were going up. |

| Printer Friendly | Permalink | | Top |

| CoffeeCat

|

Mon Dec-15-08 10:29 AM Response to Original message |

| 4. And also... |

| Printer Friendly | Permalink | | Top |

| Overseas

|

Mon Dec-15-08 12:04 PM Response to Original message |

| 8. When I watched the show I wondered if the bailout money is being saved |

| Printer Friendly | Permalink | | Top |

| girl gone mad

|

Sat Dec-20-08 09:02 PM Response to Reply #8 |

| 16. Could be, but the positive effects will be minimized.. |

| Printer Friendly | Permalink | | Top |

| sarcasmo

|

Sat Dec-20-08 01:06 PM Response to Original message |

| 11. Let us not forget about the most terrible loan of them all, the NINJA loan. |

| Printer Friendly | Permalink | | Top |

| Citizen Number 9

|

Sat Dec-20-08 01:33 PM Response to Reply #11 |

| 12. "No Income"? How common were these loans, actually? |

| Printer Friendly | Permalink | | Top |

| northernlights

|

Sun Dec-21-08 07:48 PM Response to Reply #12 |

| 17. more common than you'd think |

| Printer Friendly | Permalink | | Top |

| Citizen Number 9

|

Sun Dec-21-08 09:44 PM Response to Reply #17 |

| 18. That sorta supports what I've been saying about the mortgage meltdown |

| Printer Friendly | Permalink | | Top |

| Mike 03

|

Sat Dec-20-08 05:06 PM Response to Original message |

| 13. Yes, but I didn't know this was still a surprise. What worries me now is the pending |

| Printer Friendly | Permalink | | Top |

| Citizen Number 9

|

Sat Dec-20-08 05:24 PM Response to Reply #13 |

| 14. Exactly |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Thu Dec 26th 2024, 06:23 PM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Topic Forums » Economy |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC