At a bargain-basement auction of foreclosed homes held on Jan. 29 in a New York City Sheraton hotel, one of the music tracks that played as bidders prepared to pounce on distressed properties was James Brown's "Living in America." It was either a major planning blunder or a brilliant thematic choice. Either way, the song's lyrics ("everybody's working overtime ...") were a strangely fitting sound track to a new American reality: while corporate profits rise and economic growth returns, the housing market is only getting worse.

The latest figures from the Case-Shiller home-price index, showing a fifth straight month of price decreases including major drops in cities such as Boston, Washington, Las Vegas and Dallas have economists worried that we may be headed for a double dip in the housing market this year, which could restrain the economic growth we're finally starting to see. And 2011 was supposed to be the year housing recovered; now, analysts are betting on anything from a 5% to 20% price decline.

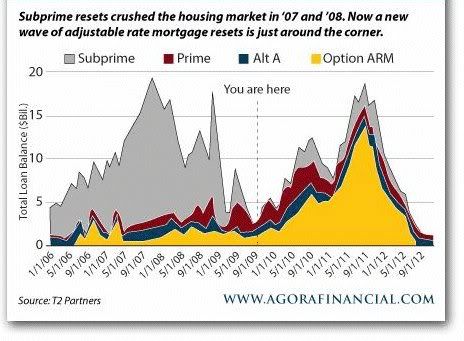

A rising number of foreclosures, tied to persistently high unemployment, is smothering housing's rebound. According to the Mortgage Bankers Association, there are already 4.5 million homes in some stage of foreclosure. Some experts believe an additional 1.5 million may be added to the pile this year. With that kind of distressed inventory on the market, it could take four to five years for prices to come back up, according to Capital Economics senior U.S. economist Paul Dales.

What's particularly troubling is that data suggests a good number of those properties belong to lower-income, higher-risk borrowers who had already gotten a break on their mortgage payments via federal programs designed to reduce defaults. November data (the latest available) on these so-called modified loans showed that 45% of them had been canceled, meaning that the borrowers very likely redefaulted, even after the payments had been adjusted.

Read more:

http://www.time.com/time/business/article/0,8599,2045854,00.html#ixzz1DNHUBY69