(Strange how often that caveat applies to your posts)

18B have been locked in by legislation, the rest isn't allocated by budget legislation yet.

It is also a foregone conclusion that this "experiment" is a failure. The history of the legislation authorizing this round of subsidies for nuclear is based on the bullshit claim by the nuclear industry that they can become a purely market financed source of power at the end of the subsidies.

That is already known to be a goal that they cannot achieve.

50 billion in nuclear loan guarantees means represents a $60 billion (plus interest on that amount amortized over 60 years) diversion of funds through the nuclear energy industry with a 50/50 chance of default on loans for those plants if the electricity is sold at market rates.

CBO estimate on nuclear loan guarantees

For this estimate, CBO assumes that the first nuclear plant built using a federal loan guarantee would have a capacity of 1,100 megawatts and have associated project costs of $2.5 billion. We expect that such a plant would be located at the site of an existing nuclear plant and would employ a reactor design certified by the NRC prior to construction. This plant would be the first to be licensed under the NRC�s new licensing procedures, which have been extensively revised over the past decade.

Based on current industry practices, CBO expects that any new nuclear construction project would be financed with 50 percent equity and 50 percent debt. The high equity participation reflects the current practice of purchasing energy assets using high equity stakes, 100 percent in some cases, used by companies likely to undertake a new nuclear construction project. Thus, we assume that the government loan guarantee would cover half the construction cost of a new plant, or $1.25 billion in 2011.

CBO considers the risk of default on such a loan guarantee to be very high�well above 50 percent. The key factor accounting for this risk is that we expect that the plant would be uneconomic to operate because of its high construction costs, relative to other electricity generation sources. In addition, this project would have significant technical risk because it would be the first of a new generation of nuclear plants, as well as project delay and interruption risk due to licensing and regulatory proceedings.

Note the price - $2.5 billion was to be only for the first plant. Future plants were, according to the assumptions provided by the nuclear industry, expected to have

lower costs as economy of scale resulted in savings.

In fact, since the report was written (2003), the estimated cost has risen to an average of about $8 billion.

Wonder what that does to the �risk is that � the plant would be uneconomic to operate because of its high construction costs, relative to other electricity generation sources�?

Does that risk diminish or increase when the price rises from $2.5 billion to $8 billion?

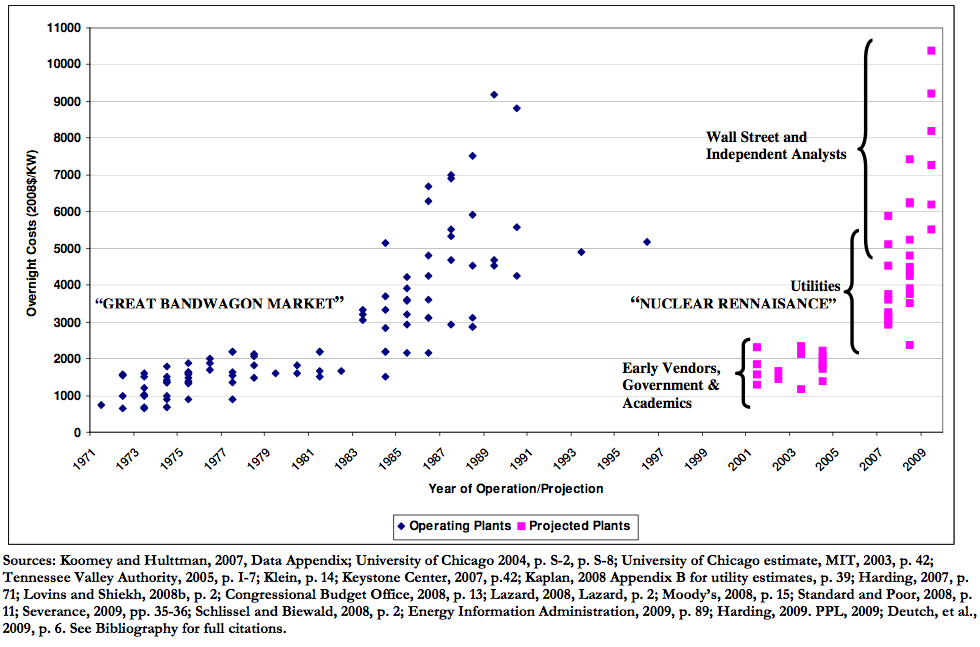

Note in the chart below the source of the various estimates for the costs of nuclear.

Early vendors, academics (who are relying on uncorrected data from those vendors) and

government (who are also relying on uncorrected data from the vendors) are ALL clearly working within a paradigm that is divorced from reality.

This paper demonstrates how independent analysis is getting it right when the insiders within the nuclear industry (which includes the utilities) are getting it wrong. The prediction the IEER paper was shown by events to be completely correct.

http://www.ieer.org/reports/nuclearcosts.pdf